New Opportunities for Banks

In recent years, the concept of embedded finance has reshaped the traditional banking and payments landscape. This innovative approach allows non-financial companies to integrate financial services into their platforms, providing a seamless experience to consumers. From major players like Amazon and Uber to smaller businesses, embedded finance is democratizing access to financial services. But what role do banks and third-party vendors play in this evolving market, and how can technology solutions help facilitate this transformation?

Understanding Embedded Finance

Embedded finance essentially enables companies to incorporate banking services—such as payment processing, lending, or insurance—directly into their non-banking platforms. This integration provides a more cohesive user experience, making financial transactions as straightforward as ordering a ride or buying groceries online.

For example, platforms like Robinhood have changed the way people invest and manage their finances by merging brokerage, banking, and retirement accounts through user-friendly interfaces. This not only simplifies user interaction but also enhances customer loyalty and service utilization.

The Role of Banks and Third-Party Vendors

Banks and third-party vendors are central to the embedded finance ecosystem. They provide the necessary infrastructure and regulatory framework for non-financial companies to offer financial services. Banks can leverage their existing capabilities and trust to partner with fintech and other industries wishing to embed financial services into their offerings.

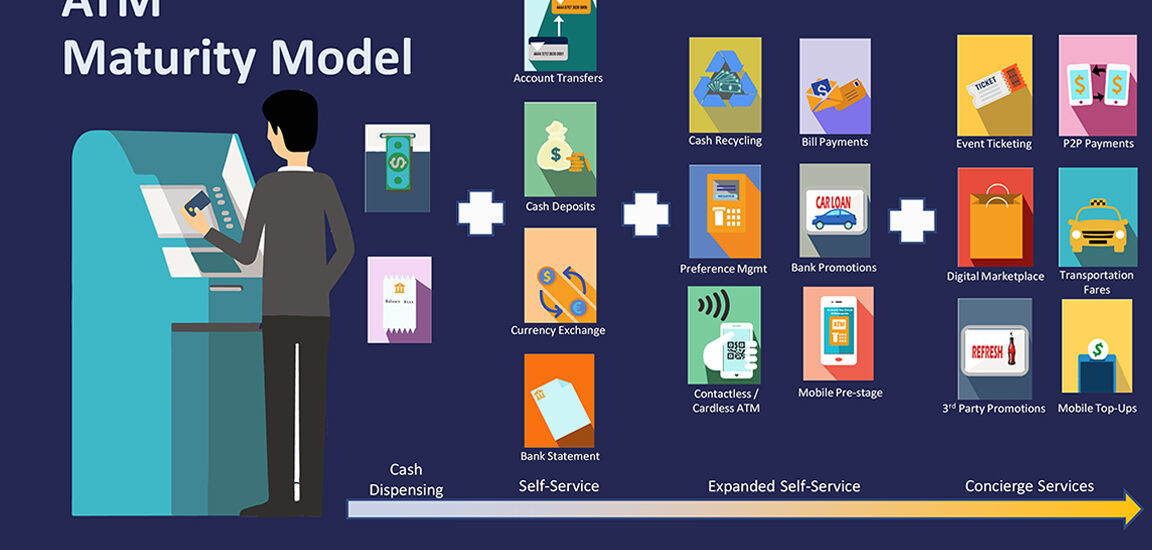

By utilizing banking infrastructure like Switching & Routing to access bank balances and safely expose them to third parties for embedded finance offerings, there is a clear pathway for banks to become integral players in providing backend solutions that support embedded finance.

The Advantages to Banks of Embedded Finance

- Increased Customer Base: By partnering with third-party companies, banks can reach a broader audience.

- Enhanced Brand Presence: When a bank’s services are embedded into a third party’s offerings, it increases the bank’s visibility and market presence without the need for extensive marketing campaigns.

- Diversified Revenue Streams: Partnering with various third parties allows banks to diversify their revenue sources. They can earn fees from third-party companies for providing banking services or earn interest from the new accounts opened through these partnerships.

- Improved Customer Engagement: Embedded finance can enhance customer engagement by providing seamless financial services within a third party’s ecosystem. Customers are more likely to use banking services if they are conveniently integrated into platforms they already use and trust.

- Cost Efficiency: Banks can save on customer acquisition costs by leveraging the customer base of their partners. The third-party companies essentially market the bank’s services, reducing the bank’s need for extensive marketing and sales efforts.

- Innovation and Flexibility: Working with third parties often requires banks to innovate and adapt their services to meet the specific needs of the partner’s customer base. This can lead to the development of new financial products and services that can be offered more broadly.

- Data and Insights: Banks can gain valuable data and insights from their partnerships, helping them understand customer behaviors and preferences better. This information can be used to tailor services and improve customer satisfaction.

- Regulatory Compliance: Banks already have the necessary regulatory frameworks in place to offer financial services. Third-party companies can leverage this compliance infrastructure to offer banking services without needing to navigate the complex regulatory landscape themselves.

- Risk Mitigation: Banks can spread risk by collaborating with third parties. For example, the financial risk associated with extending new services is shared between the bank and the partner company.

- Enhanced Customer Trust: Partnering with reputable third-party companies can enhance a bank’s credibility and trustworthiness in the eyes of consumers, particularly if the third party has a strong brand reputation.

These advantages make embedded finance a compelling strategy for banks looking to expand their reach, innovate their offerings, and enhance customer engagement and satisfaction.

How Ren Can Facilitate Embedded Finance

Euronet’s Ren Payments platform is designed to provide a robust, secure, and flexible backbone for any company looking to venture into embedded finance. Here’s how Ren could empower banks and third-party vendors:

- Modern, Flexible Technology: Ren’s platform is built with modern technology designed for flexibility to adapt to present and future embedded finance needs. Its platform-agnostic design means it can operate across various environments, whether on private or public clouds like Azure, GCP, or AWS.

- Developer-Friendly Tools: With industry-standard open APIs, Ren allows developers to easily integrate banking services into their applications, making it easier for banks and third parties to customize and extend their offerings.

- Seamless Global Payments: By bridging markets and uniting currencies, Ren helps banks facilitate faster and more efficient cross-border transactions, a critical component of global embedded finance solutions.

- Faster Market Entry: Ren’s streamlined regulations and card issuance solutions enable quicker launch times for new products, allowing banks and their partners to stay competitive and responsive to market demands.

- High Availability and Business Continuity: Ren guarantees 100% availability with its active-active+ and adaptive routing strategies, ensuring that financial services can be offered continuously, without interruption due to technical maintenance or failures.

Looking Ahead

The landscape of financial services is evolving rapidly, with embedded finance at the forefront of this transformation. For banks and third-party vendors looking to explore this burgeoning field, partnering with a technology provider like Ren can provide the necessary tools and infrastructure to successfully integrate and offer these services. By doing so, they can not only expand their market reach but also enhance the overall customer experience, paving the way for a new era of financial integration.

Engage with Euronet’s Ren API Gateway

Discover the Ren API Gateway’s transformative potential for your institution. Embrace the technology that powers seamless, secure, and efficient digital banking.

To explore how Euronet can support your digital transformation journey, contact our team, or visit us at https://euronetsoftware.com/.