More than a year has passed since the COVID-19 pandemic became part of our lives, and our “new normal” started taking shape. Changes in our social behavior led to changes in the ways we do business. We increasingly avoided physical retail stores, opted for online shopping, and converted to digital forms of payment. Consequently, the use of cash decreased significantly.

Vaccines are once again shifting the new normal, and while some recently adopted behavior will remain, there is also a return to our former lives, including the use of cash for payments. Consider:

- Consumers who were avoiding cash due to hygiene considerations are comfortable handling cash after vaccination.

- Cash is considered by many a shelter in times of crisis.

- A considerable consumer segment—the unbanked and underbanked—continue to use cash as their primary payment method.

- The post-Covid era seems to be one of less cash, rather than cash-less.

How will the ATM participate in this new financial landscape? What will be the primary purpose of ATMs in the future, and how can financial institutions adapt to ensure they are running a profitable ATM fleet?

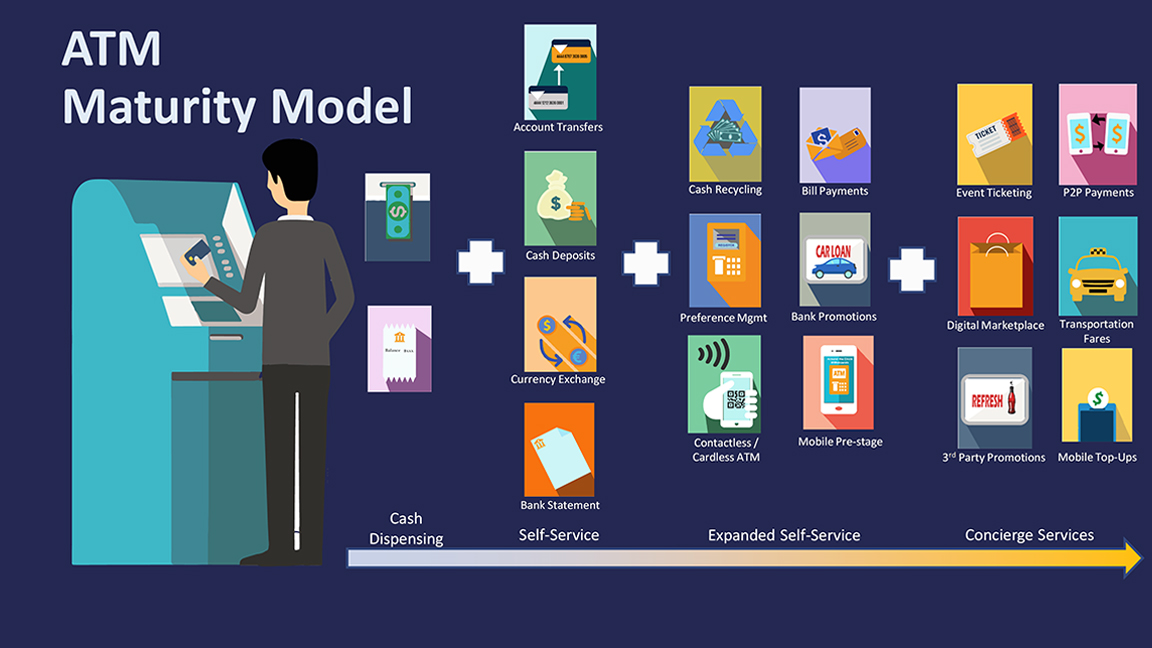

Evolution is the key to future-proofing the ATM. Even before the pandemic began, the ATM channel had started to play an expanded role, with services such as bill payments and mobile top-ups part of the offering. Now, with self-service being the preferred method of banking, it is time to extend the role of this powerful self-service channel even further—to become a digital payments and transaction hub. This transition will produce new functionality and new revenue streams that can compensate for the diminished frequency of cash withdrawals and turn the ATM channel into a revenue generator. Below are a few adaptations for your consideration:

- Cash-in transactions are gaining popularity. As the underbanked population with cash in their pockets seeks to participate in digital payments, the self-service terminal offers a way to deposit cash into prepaid wallets that may be used for online purchases or pay bills electronically.

- Consumers make purchases at the ATM. Consumers can buy tickets for events, local attractions, or public transportation, digital content cards, insurance, stamps, and prepaid cards—either plastic or virtual.

- Card-less transactions allow P2P cash payments to any beneficiary.

- Automated check deposits enhance customer service.

- Charity donations provide a simple and convenient way to support community service organizations.

- Services to travelers in airports, seaports, and train and bus terminals may include dispensing of foreign currencies or dynamic currency conversion.

- ATMs may act as a cash reward dispensing point for customer loyalty programs, B2C bonuses or incentives, or even lottery payouts.

- Advertising on ATM screens and receipts can provide additional income.

- Marketing Campaigns offer cross-selling opportunities to new and existing clients.

- Kiosk-type account services can reduce banking operating costs.

- Cash Recycling and Remote Key Loading can greatly reduce ATM maintenance expenses.

- While not a new revenue stream on their own, contactless, or less-contact transactions contribute to returning trust in the safety of ATMs.

As ATMs transform into digital payment hubs, they will gain an expanded significance for financial institutions and consumers, despite the declining demand for cash.